Market Wrap – November 18, 2025: Tech Cracks, Oil Holds, and the 10-Year Drifts But Doesn’t Break

Tech stocks dragged the market lower as the Dow fell nearly 500 points, oil held above $60, and the 10-year drifted near 4.11% in a mixed macro session.

Market Wrap – November 18, 2025: Tech Cracks, Oil Holds, and the 10-Year Drifts But Doesn’t Break

Big Tech led another wave of selling as the Dow dropped nearly 500 points and the S&P posted a fourth straight loss, even as the 10-year yield eased slightly and oil held above $60. Crypto tried to bounce after briefly breaking $90K overnight.

Cross-Market Snapshot – Tech Drag, Mixed Signals

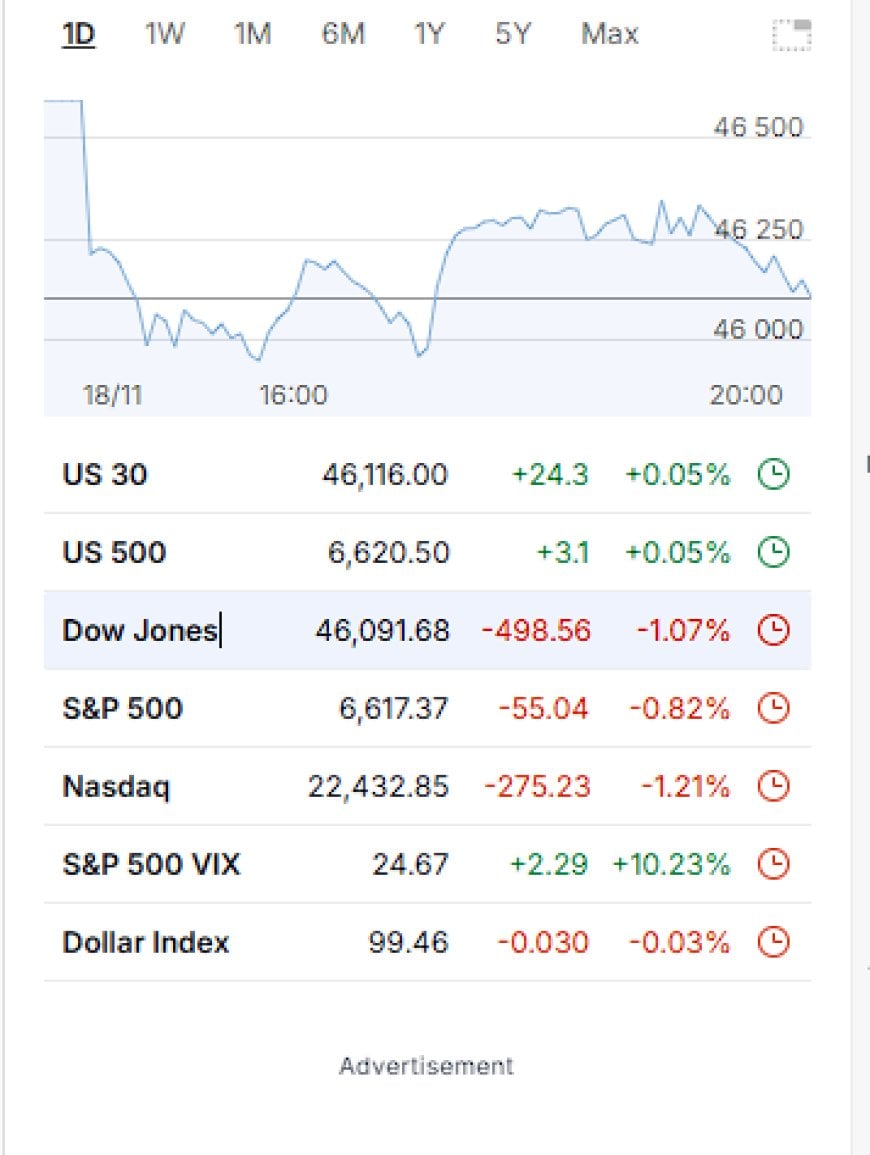

Today looked like a continuation of yesterday’s stress, but with a slightly different mix. The Dow dropped roughly 500 points (≈–1.1%), the S&P 500 fell about 0.8%, and the Nasdaq slid more than 1.2%, marking the S&P’s fourth straight daily loss.

Underneath that, the 10-year Treasury yield actually eased a bit toward the 4.10–4.12% area, while the dollar index finished roughly flat on the day. Crude oil held just above $60 a barrel, and gold managed a small green print.

So we’ve got a weird combination again: equities down, Big Tech hit hardest, bonds bid, oil stable, crypto trying to bounce. It’s not a “sell everything” liquidation, it’s a targeted de-rating of the AI/mega-cap story with the long end of the curve watching quietly.

Equities – AI Darlings Bleed, Indexes Roll Over

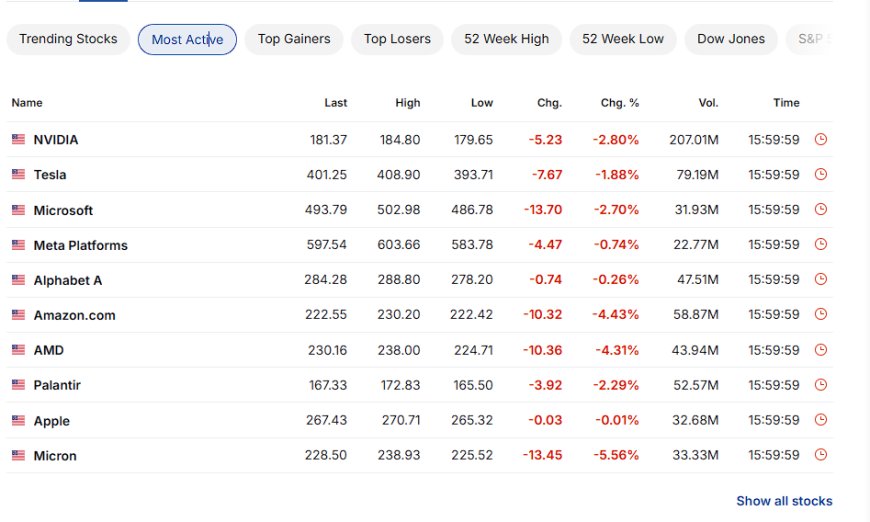

Equities once again moved in a pattern that screams “AI bubble fatigue.” Nvidia, Microsoft, Amazon, Tesla, AMD, Micron and the rest of the AI-complex traded heavy, with several of them down between 2–5% on the day as investors braced for Nvidia’s upcoming earnings and questioned stretched valuations.

The headline numbers:

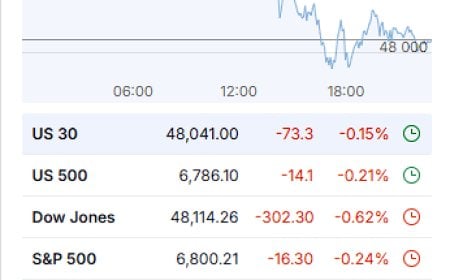

- Dow Jones Industrial Average: ~46,092, down about 498 points (–1.07%)

- S&P 500: ~6,617, down about 55 points (–0.82%)

- Nasdaq Composite: ~22,433, down about 275 points (–1.21%)

- S&P 500 VIX: pushed toward the mid-24s, up another ~10%+

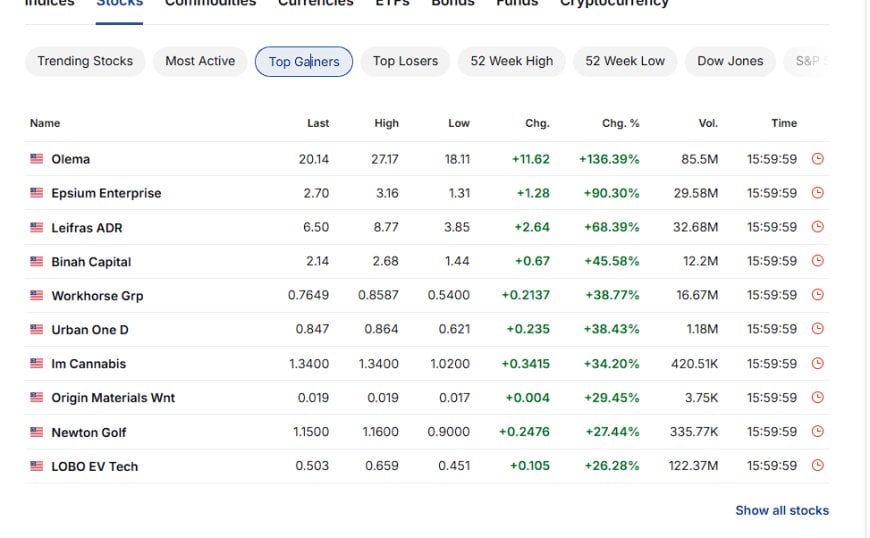

At the same time, the top gainers list showed the same micro-cap fireworks: biotechs, cannabis names, and assorted story stocks ripping 30–130% on the day. That’s classic late-cycle behavior — the index-level tape looks cautious, but sub-sectors are still playing casino.

Put simply: the market isn’t rejecting equities as an asset class yet. It’s repricing where within equities it’s willing to pay 30–40x forward earnings, and for now, AI mega-caps are on the wrong side of that adjustment.

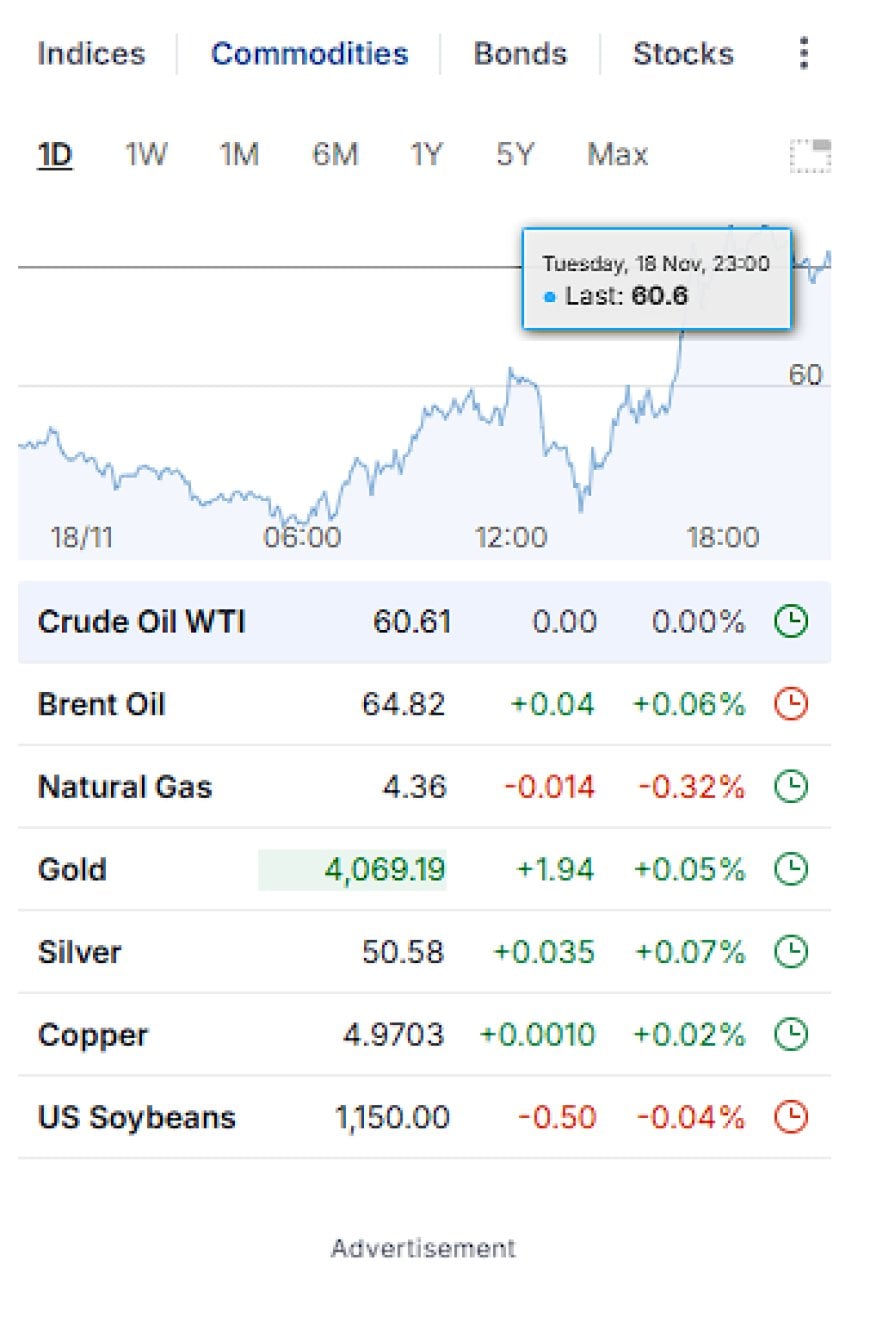

Commodities – Oil Firm Above $60, Gold Tries to Stabilize

WTI crude held around $60.5–$60.6, flat to slightly up on the session, as markets digested fresh headlines about Russian crude piling up at sea and ongoing sanctions chatter that tighten the medium-term outlook even as near-term supply worries calm.

Brent hovered in the mid-$60s, and the broader message from both EIA and OPEC over the last few days is “prices dip, but structurally tight into 2026” as inventories, sanctions, and AI-driven power demand collide.

Gold and silver printed small green candles — the kind of move that tells you there’s some demand for hedges, but not enough fear to blow open the doors. In other words: this still isn’t a gold-led panic.

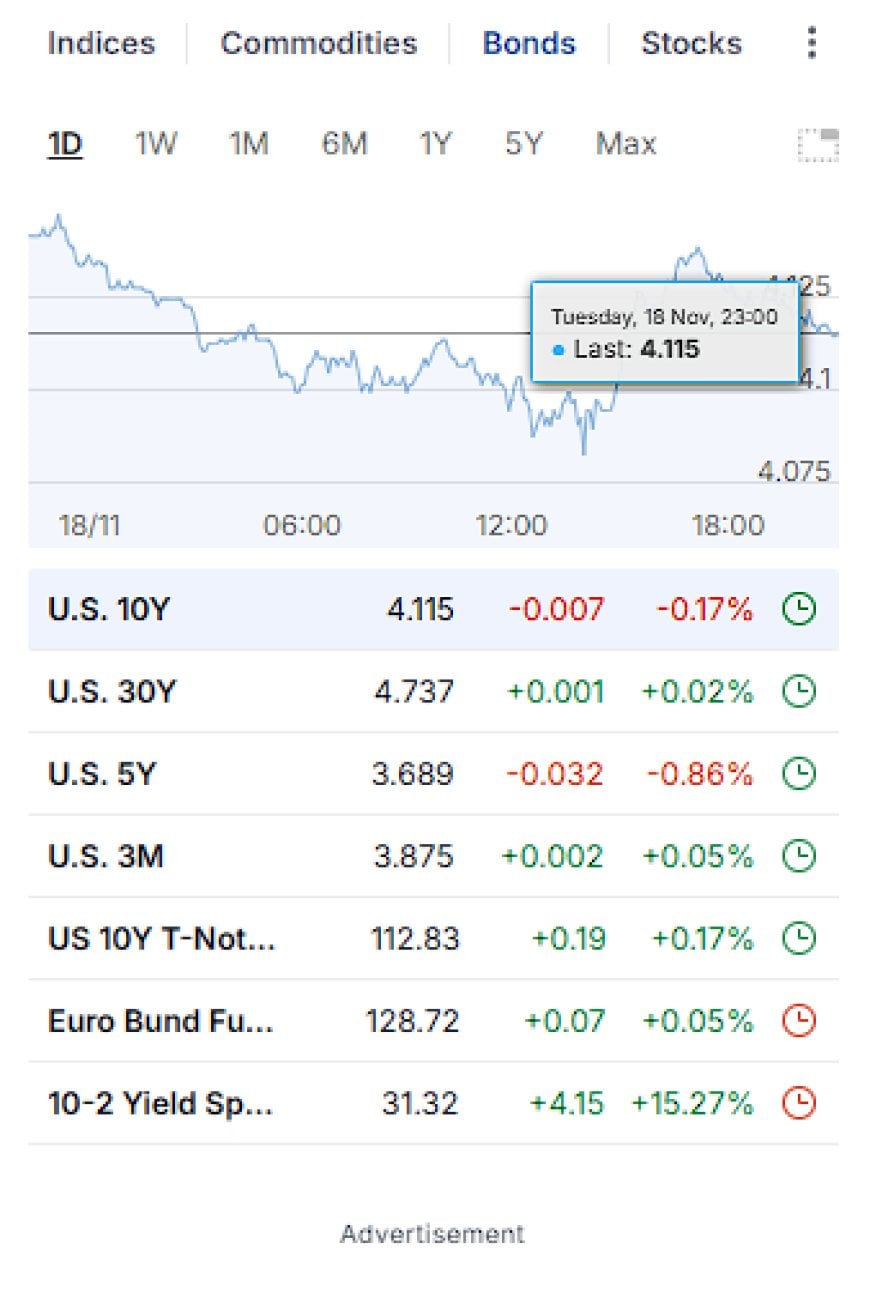

Rates & Bonds – 10-Year Softens, Term Premium Still in Charge

The 10-year Treasury yield ticked down a few basis points to roughly 4.11%, easing from yesterday’s close around 4.13%, as labor data and weaker equities drove a modest bid for safety. Shorter maturities barely moved, and the 10–2 spread stayed in its recent positive-but-shallow steepening range.

This is important: the move lower in yields is orderly. We’re not seeing a full “growth scare” collapse in the long end; we’re seeing a market that already repriced to higher-for-longer now nudging yields down at the margin as tech corrects and data softens.

The term premium is still doing the talking. Fiscal deficits, issuance, and the AI–power buildout haven’t gone anywhere. A 10-year at ~4.1% with equities wobbling is the market saying: “we’ll entertain cuts at the front end, but the cost of time stays elevated.”

Dollar & FX – Flat Tape, No Panic Bid

The dollar index (DXY) finished roughly flat to marginally down around the high-99s. There was no big “dash to dollars” despite the selloff in equities.

That combination — equities lower, yields slightly lower, dollar basically unchanged — fits with the idea of a valuation adjustment, not a global liquidity shock. Foreign FX markets mostly tracked that benign story, with only modest moves in the euro and yen.

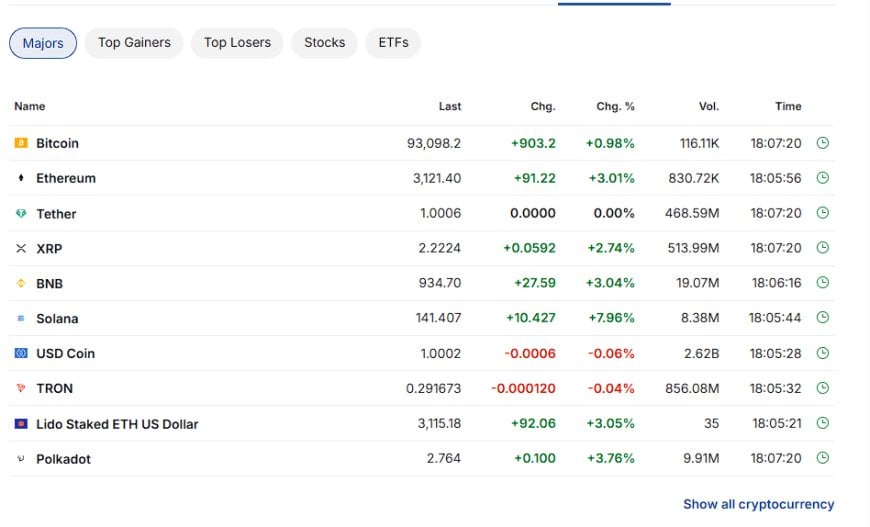

Crypto – Bouncing After a Breakdown

Overnight, Bitcoin finally cracked: it briefly traded below $90,000, wiping out all of its 2025 gains and leaving it more than 25–30% off the October high above $126K. That move triggered a swarm of “death cross” and “end of the cycle” headlines.

By cash close in the US, BTC had clawed back toward the $92–93K band, up about 1% on the day from the intraday low. Ethereum and Solana bounced harder, posting 3–8% gains from the bottom as speculative flows tried to pick a short-term low.

The bigger story is that crypto is now trading like a high-beta macro asset again. The same valuation anxiety hitting AI mega-caps is bleeding into the “digital risk” complex — and as several research desks pointed out today, prior Bitcoin drawdowns of this size have often coincided with broader risk-off phases.

Structural Pattern – De-Rating the AI Story, Not the System

Zoom out from the tick charts and the pattern is consistent with the AI-industrial, higher-capex regime I’ve been mapping out:

- AI mega-caps are being forced to prove that earnings can catch up to narrative. The market is no longer willing to pay pure story multiples with 4–4.25% on the 10-year.

- Bond markets are not screaming crisis; they’re moderating yields while keeping term premium alive, which is exactly what you’d expect when capex and deficits stay high.

- Oil holding ~$60 alongside sanctions, data-center power demand, and underinvestment in new supply reinforces that the energy side of the AI buildout is still underpriced.

- Bitcoin’s slide isn’t yet about the failure of digital rails — it’s about speculative layers getting repriced while stablecoins and tokenized Treasuries quietly deepen their roots.

In other words, the market is re-rating the equity and crypto stories sitting on top of the system, not rejecting the system itself. The plumbing — dollar, Treasuries, energy, AI capex — remains the foundation.

Key Levels I’m Watching

- S&P 500: 6,550–6,600 as the short-term support band. We’re closing right on top of it; a clean break opens the door to something more than a 5% pullback.

- Dow: 46,000 — today’s close just above that level is psychological more than technical, but a sustained move below would confirm a deeper de-risking.

- 10-Year Treasury: 4.0% on the downside, 4.15% on the upside. A decisive move either way will tell you whether this is just noise or the start of a new regime leg.

- Bitcoin: $90K as the line in the sand. Holding above suggests consolidation; losing it again with size points toward a deeper flush into the $75K area the street is now whispering about.

- WTI crude: $60 remains the pivot point between “too cheap given AI + geopolitics” and “growth scare.”

What to Watch Next

Over the next 24–72 hours, the focus stays tight on:

- Nvidia earnings: the market’s referendum on whether the AI capex boom can justify current valuations.

- Incoming labor and inflation data: any further softening in jobs or prices pulls the 10-year closer to 4%; a surprise re-acceleration pushes it right back up.

- Crypto follow-through: does Bitcoin stabilize above $90K and build a base, or does the overnight break turn into a proper capitulation?

Bond Market Outlook – The Pattern Nexus View on the 10-Year

Beneath the noise of red days, tech selloffs, crypto whipsaws, and commodities grinding sideways, the most important signal in the system remains exactly where it’s been for months: the U.S. 10-year Treasury.

Today’s move was small — drifting a few basis points lower into the 4.10–4.12% range — but the significance isn’t in the print. It’s in the behavior. The 10-year refuses to break down, refuses to reprice toward the Fed’s dovish forward guidance, and refuses to validate a 2026 “clean-cut” narrative.

The Pattern Nexus framework holds that the 10-year is no longer a reflection of short-term policy hopes. Instead, it’s becoming a structural barometer of three forces:

- 1. AI-Driven Capex Pressure — The data center buildout, grid reinforcement, transmission upgrades, SMR projects, and the expansion of power-intensive industries are keeping real rates elevated. Capital has a cost again.

- 2. Permanent Fiscal Heavyweighting — Deficits, defense spending, Treasury issuance, and entitlement spending have created a world where term premium isn’t an anomaly — it’s the baseline. The long end is demanding compensation for structural uncertainty.

- 3. Global Liquidity Realignment — As the world reorganizes around tokenized Treasuries, dollar rails, stablecoins, and cross-border settlement infrastructure, the 10-year becomes the center of gravity. Not the Fed Funds rate. Not SOFR. The 10-year is becoming the new anchor of global collateral pricing.

That’s why the tape feels “off” to so many observers. Stocks can fall, oil can rally, crypto can bounce, metals can drift — and the 10-year just sits stubbornly in the low 4s, refusing to break down.

In Pattern Nexus terms, this is the defining signal of the transition into 2026: a world where interest rates stop following policy forecasts and instead reflect the physical, fiscal, and energy-based constraints of a newly industrializing AI-driven economy.

As long as the 10-year stays above the psychological 4.00% floor, the market hasn’t returned to “easy money,” regardless of what the Fed says. The long end is sending its own message: this is a higher-duration-cost world, and the price of time is structurally repriced.

Watch this level more than any index, commodity, or crypto chart. The 10-year is the quiet metronome of the new macro regime — and it’s nowhere near finished speaking.

Consumer & Real-Economy Stress Signals – The Quiet Early Warning

One thing I want to layer on top of today’s action — and it sits beneath every chart above — is the real-world financial stress that isn’t showing up in official data yet.

I’m seeing it directly through my tenants: more people asking for extensions, more partial payments, more “can I pay you Friday instead?” conversations. These are people who have never been late in two or three years suddenly losing their buffer.

That may sound anecdotal, but historically, consumer stress always shows up at the bottom first — long before the big banks, the indexes, or the government data acknowledge it.

And here’s why that matters right now: if holiday retail — Black Friday, Cyber Monday, December spending — comes in weaker than expected, it will feed directly into:

- a deeper de-rating of Big Tech and AI valuations

- pressure on the S&P 500’s earnings assumptions

- a bond-market bid that pulls the 10-year toward that critical 4.00% level

- a broader “risk recalibration” across crypto and high-beta assets

That’s the real pivot point: consumer weakness + AI valuation stress + a coiling 10-year yield = a market positioned for a bigger correction if the next data releases disappoint.

Conversely, if Nvidia confirms the AI capex boom and holiday spending comes in resilient, the 10-year breakout coil snaps the other way — and the entire market gets a relief rally into month-end.

This is the hinge between two paths, and the bond market is already telling you it’s preparing for whichever one hits first.

Core Reading Path

- The AI Industrial Flywheel

- The New Dollar Hierarchy: Stablecoins, CBDCs & Global Liquidity

- The Tokenized Reserve Era

Related Market Analysis

- Market Wrap – November 17, 2025

- The Quiet Crisis: Rising Foreclosures & Falling Rents

- Why the 10-Year Treasury Isn’t Listening to the Fed

- Stablecoin Geopolitics & the Coming Digital Dollar Era

Energy, AI & Power Infrastructure

- AI, Power Grids & the New Energy Bottleneck

- AI’s Nuclear Backstop: Powering the Compute Boom

- America’s New Map of Power (Data Centers & Grid Shortfall)

Global Liquidity & Macro Mechanics

Pattern Nexus Deep Research

- The U.S. Fiscal Supercycle

- The AI Capex Supercycle

- Yield Curve Reconstruction & the 2026 Regime Shift

Latest From Pattern Nexus

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Founder of Pattern Nexus. I research markets, macro, geopolitics, AI, history, ancient systems, and the patterns most people overlook. I’m also building Market Radar, a trading scanner designed to read pressure, risk, confirmation, and setup quality before chasing a move. Pattern Nexus is where I connect the dots between data, history, technology, and the bigger system playing out around us.

Comments (0)